-1920x700.png)

How to Respond to a Defective Return Notice?139-(9)

If the return is lacking crucial information or was incorrectly recorded in the ITR, a faulty return notification can be issued under Section 139(9).

It is common to omit information or make errors while filing income tax forms. These errors render your return "defective," and you will receive a defective return notice under section 139(9). Section 139(9) of the Income Tax Act of 1961 stipulates that if a return is deemed to be incorrect, the A.O. will allow you 15 days to fix the error. The return can be regarded as defective for one of several reasons, as listed below.

Budget 2024 Update

FM Nirmala Sitharaman has made two announcements for those opting for the new tax regime.

First, the standard deduction for salaried employees is proposed to be increased from Rs 50,000/- to Rs 75,000/-. Similarly, deduction on family pension for pensioners is proposed to be enhanced from Rs 15,000/- to Rs 25,000/-.

Second, in the new tax regime, the tax rate structure is proposed to be revised, as follows:

0-3 lakh rupees - NIL tax

3-7 lakh rupees - 5% tax

7-10 lakh rupees - 10% tax

10-12 lakh rupees - 15% tax

12-15 lakh rupees - 20% tax

Above 15 lakh rupees - 30% tax

As a result of these changes, a salaried employee in the new tax regime stands to save up to Rs 17,500/- in income tax.

What is a Defective Return?

A defective return occurs when any critical information is missing or incorrectly recorded on the return form. In any of the aforementioned circumstances, the income tax department provides a faulty notice to the taxpayers under Section 139(9), informing them of the situation and requesting that they correct the inaccuracies in the return.

You must submit the appropriate adjustments to the return within 15 days of receiving the notice. Failure to correct the ITR on time may have long-term ramifications.

The defective return notice under section 139(9) is sent via email to your registered email address. You can also get the notice using the income tax e-filing system.

What is the Reason for Defective Notice 139-9?

- Incomplete ITR - The income tax return's annexure, statements, and columns must all be filled out. It must be filled out exactly as requested. For example, when claiming a deduction under Section 80G, the details in the schedule must be filled out or correctly completed.

- Missing Tax Information - Tax and interest, if any, are paid prior to filing the return, but all relevant facts are not filled in. For example, the BSR code, challan date, and serial number should all be right.

- Mismatch in Information - The tax actually paid does not correspond to the tax payable on the income tax return, or taxes are not paid in full.

- Presumptive Taxation Scheme - When submitting ITR 4, if total presumptive income is less than 8% or 6% of gross turnover or receipts, respectively, ITR 3 should be filed. The gross receipts are not mentioned in the profit and loss account, or the gross receipt or revenue under section 44AD is shown as greater than Rs. 2 crore in ITR 4.

If you filed your return under Section 44ADA with a gross receipt of more than 50 lakhs but did not include a balance sheet or profit and loss statement, you will receive a notice to file ITR-3 with an audited balance sheet and profit and loss statement.

This presumptive taxes ceiling was doubled in the 2023 budget. 44AD is increased to 3 crores, whereas 44ADA is increased to 75 lakhs. This increase in limit is subject to the condition that 95% of receipts are from online sales.

- Maintaining books of account - You are expected to keep regular books of account, such as balance sheets and profit and loss statements, but they were not included in the return when it was filed.

- TDS Claimed but Income Not Mentioned: The tax deducted has been claimed as a refund, but no income information is offered in return.

- Relevant to Income Tax Audit - When the books of accounts have been audited but a copy of the audit report and audited financial statements have not yet been filled out and filed with the return.

- Cost Audit Requirements: If the entity is obligated to conduct a cost audit but fails to provide detailed information about it.

- Mismatch in Name: There is a name mismatch between PAN and Income Tax Return.

What should I do after receiving notice under section 139(9) of income tax act?

Once you have received an income tax notice under Section 139(9), you must revise your return within 15 days of receiving it from the Income Tax Department. You can also petition for an extension by writing to the Assessing Officer (A.O.) and requesting that the time for filing a revised return be extended. Practically speaking, even if a taxpayer corrects the defect after the fifteen-day period has expired. However, before the assessment is conducted, the Assessing Officer may excuse the delay and accept the return as legitimate.

However, if the response is not filed within 15 days or if an extension is granted, the initial return is considered invalid.

What Happens If I Do Nothing After Receiving a Notice for Defective Return Under Section 139(9)?

Your defective return will be considered a non-filed or invalid return. This means that the Income Tax Department will treat it as if you had not filed a return for the year. As a result, any refund you get will not be processed by the Income Tax Department.

How Will I Receive Notice under Section 139(9)?

The income tax department will send you a notice under Section 139(9) via the email address you provided when filing your ITR. Typically, these notices are sent from CPC with the subject line 'Communication u/s 139(9) for PAN AWZXXXXXXX for the A.Y.2023-24'. The warning is attached to the email and password-protected. The password to open the notification is PAN in lowercase and your date of birth in the format DD/MM/YYYY.

How to Respond to a Notice under Section 139(9)?

Here's how to reply to income tax notices:

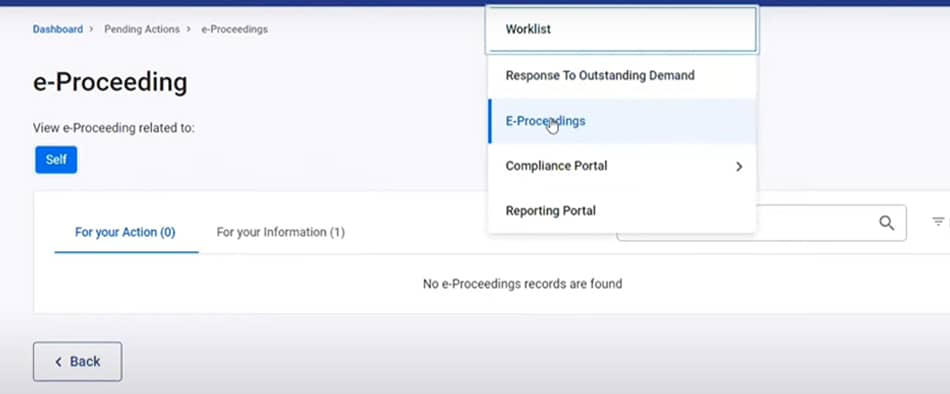

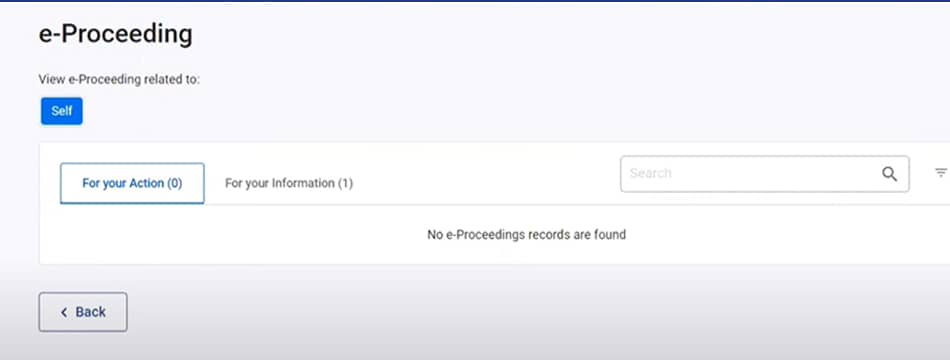

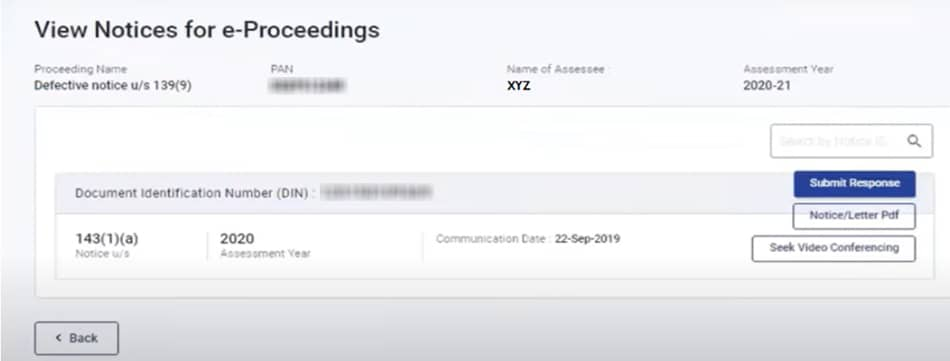

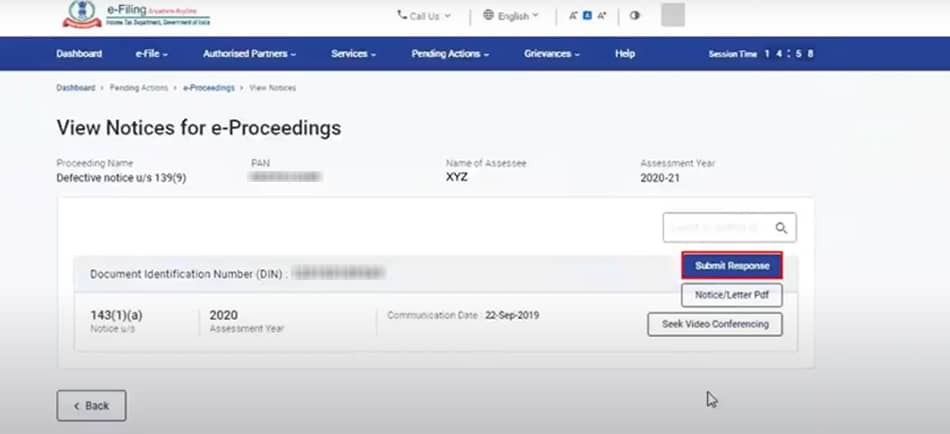

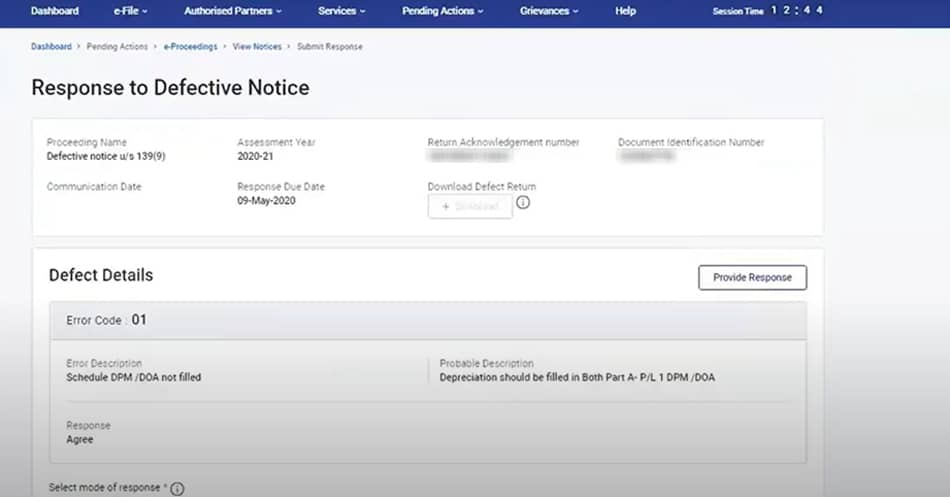

Step 1: On the dashboard, click on pending actions, then e-proceedings.

Step 2: If you have not received any notice, you will see No e-proceedings records

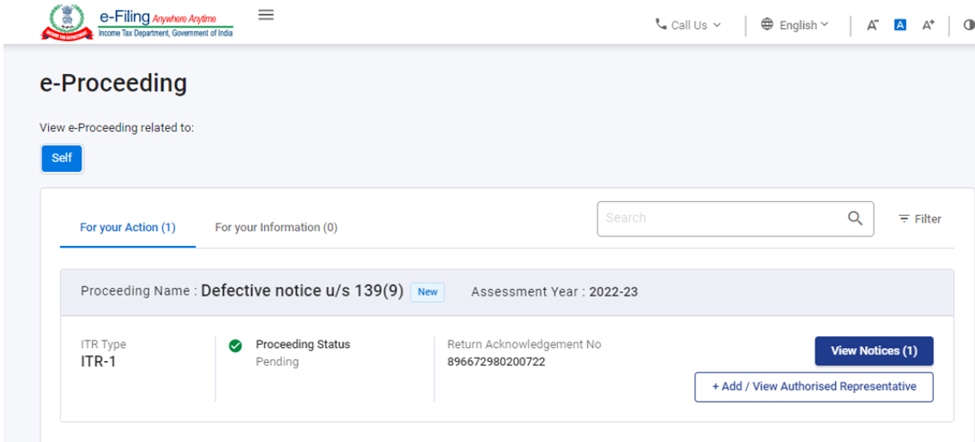

Step 3: If there is any proceeding, you will see it in your pending actions.’ Click on ”For your action and view Notices

Step 4: Click on ‘Notice/ Letter pdf’ to view the notice.

Step 4 (A): After you have viewed your notice, click on submit a response.

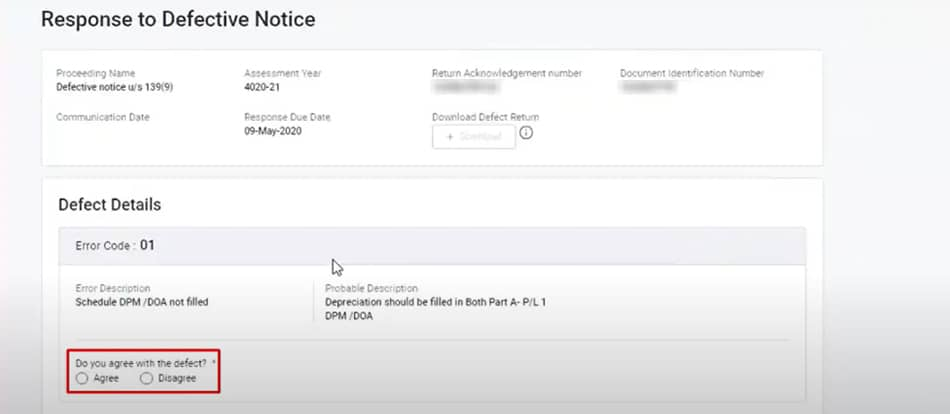

Step 5: After you have clicked on submit a response, you will see a response page where you will have to agree or disagree with the notice.

Step 6: If your response is ‘agree,’ you will see a screen where you will have to provide a response for the said defect.

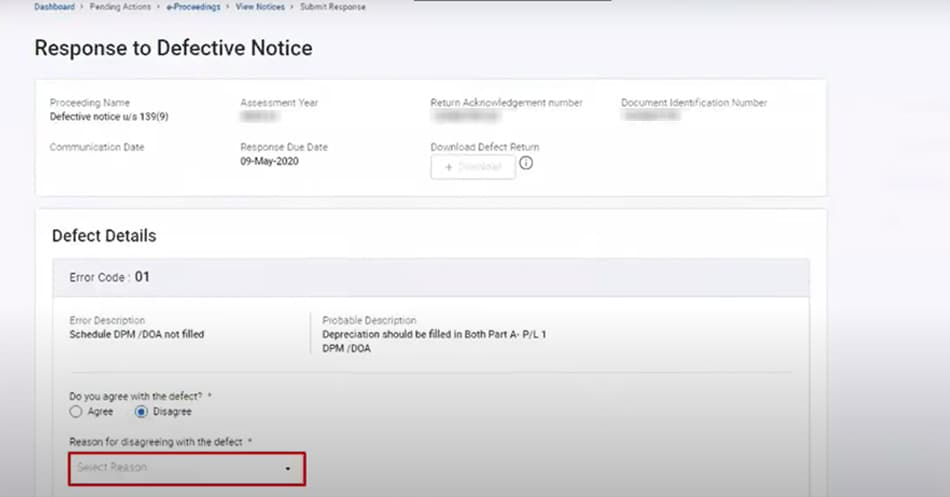

Step 6 (A): If you disagree with the notice, you can select disagree in the given column and give reasons for the disagreement in the text box provided.

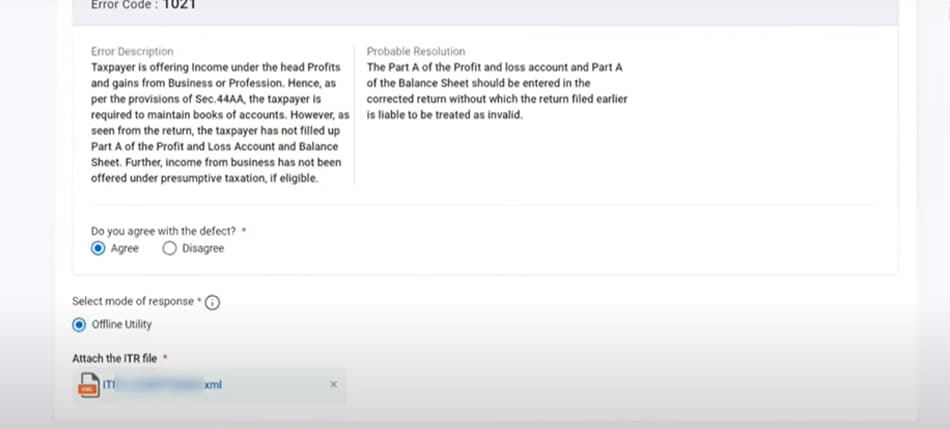

Step 7: Now, if you have selected the agree-on option and offline utility as the mode of response, submit the attachment file for rectifying the defect.

Time limit for responding to defective notice.

If you get a defective notification, you have 15 days from the date of receipt or as described in the notice to correct the defect in the return you filed.

Can I withdraw my response to a defective notice under section 139(9)?

Previously, it was allowed to withdraw your response to the defective notification under section 139(9). However, this capability is no longer available. As a result, you cannot remove your response; however, you can change or see it.

How Do You Revise Your Income Tax Return in Response to the Notice?

Receiving a tax notice should not generate panic or stress. Instead, use it as an opportunity to correct errors in your original income tax return. Section 139(5) of the Income Tax (IT) Act allows taxpayers to modify their IT returns. This clause enables taxpayers to correct any inadvertent errors or omissions in their IT returns, even after getting a tax notice under Section 139 9 of the Income Tax Act. The revision can be done before one year has passed since the conclusion of the relevant assessment year or before the assessment year is completed, whichever occurs first. This flexibility allows taxpayers to correct mistakes and assure.accuracy in their tax filings.

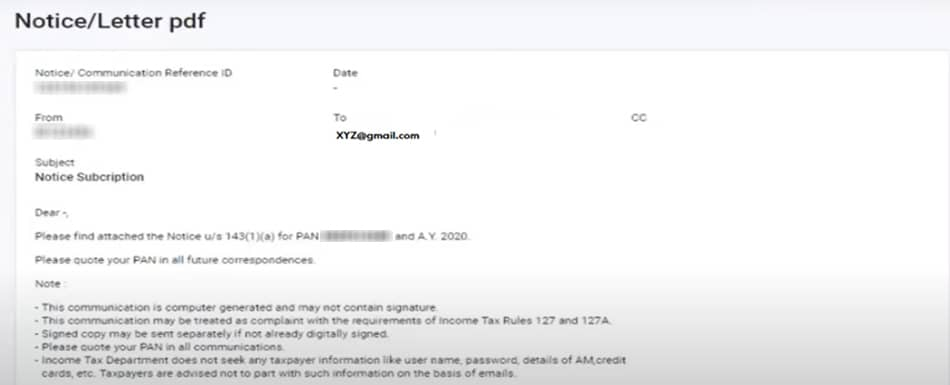

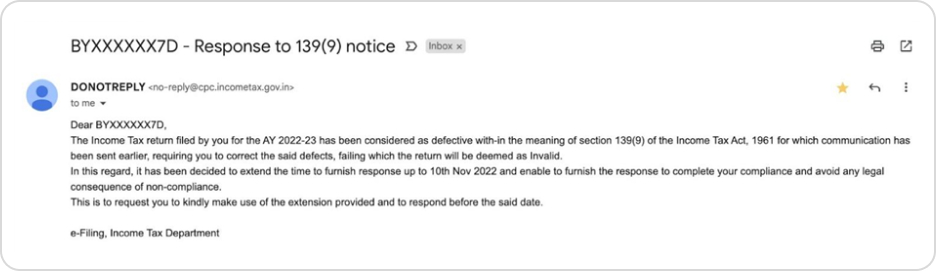

Sample email of the Notice under Section 139(9)

FAQs on Notice for defective return u/s 139(9) of the Income Tax Act

Q.How will I receive the defective notice from the IT department?

You will receive an email from the IT department with the subject line "Important - Rectify the defect in your Return of Income." The department also sends an SMS alert to the tax filer stating that the notification notice has been issued to their registered email address.

Q.How can I reply to a notice under Section 139(9) when the tax payable exceeds the tax paid in return received from the Income Tax Department?

This issue arises when the tax payable on the return filed exceeds the tax paid. To correct this error, the tax should be paid in full with interest to the Income-tax department on the corrected return.

Q.Why does my ITR status indicate that 'no further action is necessary since the latest return is taken for processing'?

It signifies the return is error-free, with all faults removed and ready for processing

Q.How can I pay the remaining income tax after obtaining notification under section 139(9)?

To pay the remaining income tax under Section 139(9) of the Income Tax Act, 1961:

- Pay taxes online, just like you would for self-assessment taxes.

- Submit your amended result and generate JSON L for it.

- Then log in to the income tax portal.

- Go to the dropdown menu and pick e-file response u/s 139(9).

- Examine the JSON generated in the response.

- An amended return and response under section 139(9) was filed.

Q.Invalid returns u/s 139(9). Can I file it again as a new return for that year?

When a return is determined to be defective, a notice is issued under Section 139(9) of the Income Tax Act, and the assessee is given 15 days to rectify the matter; however, if the assessee fails to do so, the return is declared defective and handled as if it was never filed. If the assessee wishes to file a return later, he may do so by submitting a belated return.

However, the deadline for overdue returns is three months before the end of the applicable Assessment Year. For example, the ITR for FY 2021-2022 can be filed up to December 31, 2023.

In response to 139(9), I submitted an amended Income Tax Return. Do I need to react to 139(9) separately?

Normally, Compliance can be submitted with the Disagree option, indicating that the Return has been revised. However, the action may differ depending on your specific circumstance, for which our Tax Experts can provide more assistance.

Q.I have got notification under section 139(9). My Form 26AS reflects additional pension income received from the Army. Please let me know if it's taxable. I'm currently receiving Form 16 for another employment.

If you receive a lump-sum pension from the armed forces, it is completely exempt. However, if you receive a periodic pension from the armed forces, it is taxed. Furthermore, the lump sum pension received by military family members is completely exempt. As a result, you can respond to the notification appropriately.

Q.What is Section 139(9) of the Income Tax Act?

If incomplete or incorrect information is provided while filing an income tax return, the assessee would receive a notice under Section 139(9) of the Income Tax Act. You have 15 days to reply to this notice. If the assessee fails to react to the notice, they can request an extension of the deadline by writing a letter to the department.

Q.When does the Income Tax Department issue a notification under Section 142?

The income tax department may issue a notification under Section 142(1) if you have not filed your income tax return for the relevant assessment year or if the Assessing Officer requests additional information or documents.

You must file such a return within the time frame specified in the notice, or provide such documents and information as requested by the Assessing Officer.

Q.What will happen if you do not answer to notice u/s 139(9)?

If you fail to respond to a defective return notification in a timely manner, your ITR for the relevant assessment year will be declared invalid. You will have to face the repercussions, such as a penalty, interest, the inability to carry forward losses, and the loss of special exemptions.