-1920x700.png)

Income Tax Slabs FY 2023-24 & AY 2024-25: New & Old Rates

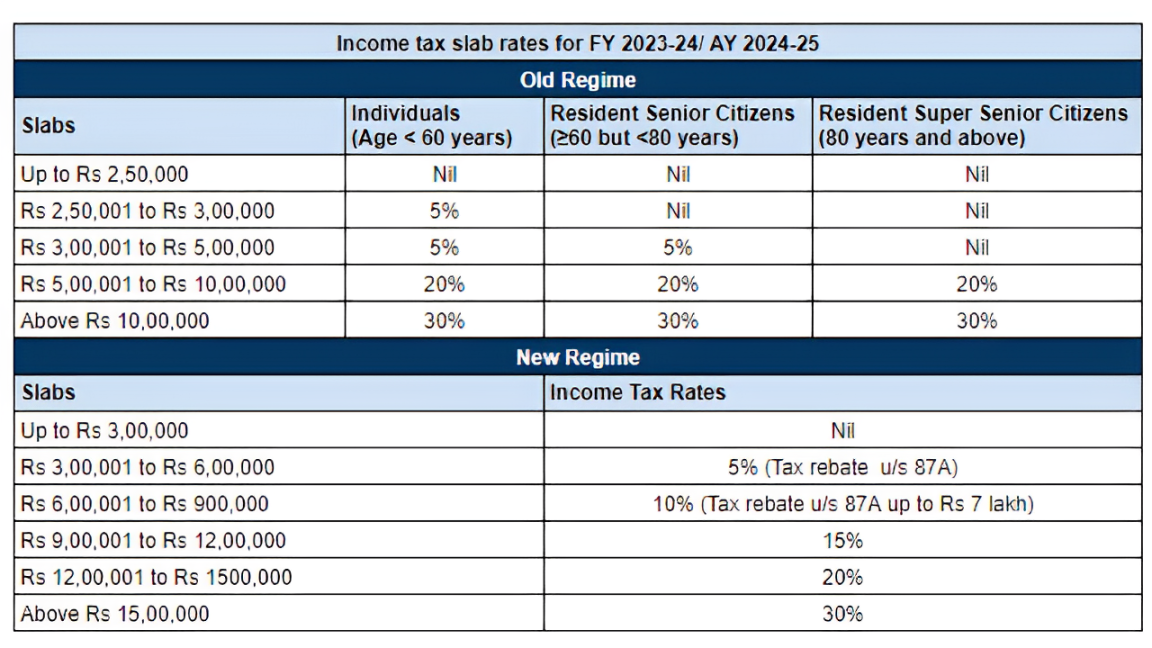

The income tax slabs differ significantly between the old and new tax regimes. Under the old tax regime, the slab rates are categorized into three groups based on age and residency:

- Indian Residents aged < 60 years: This category includes all Indian residents who are below 60 years old.

- Resident Senior Citizens (60-80 years): This category includes Indian residents who are 60 years or older but less than 80 years old.

- Resident Super Senior Citizens (> 80 years): This category includes Indian residents who are 80 years or older.

Interim Budget: 2024-2025 Update: The Interim Budget 2024-2025 did not include any changes to direct taxes.

What is Income Tax slab in India?

the Income duty is levied on people using an arbor system, with different duty rates assigned to different income situations. duty rates rise in proportion to an existent's income. This kind of taxation allows for a further indifferent and progressive duty structure in the country. Income duty classes are streamlined on a regular basis, generally around budget season. The arbor rates differ for different types of taxpayers.

Let us take a look at all the slab rates applicable for FY 2023-24(AY 2024-25)

Under the Old Tax Regime:

- Individuals and Hindu Undivided Families (HUFs) below 60 years old and NRIs have an income tax exemption limit of up to Rs 2,50,000.

- Senior citizens (aged 60 years or more but less than 80 years) have an exemption limit of up to Rs 3,00,000.

- Super senior citizens (aged 80 years or more) have an exemption limit of up to Rs 5,00,000.

- A tax Slab of up to Rs 12,500 is available if total income does not exceed Rs 5,00,000 (not applicable for NRIs).

Under the New Tax Regime:

- Individuals and HUFs opting for the new regime have an income tax exemption limit of up to Rs 3,00,000.

- A rebate of up to Rs 25,000 is applicable if total income does not exceed Rs 7,00,000 (not applicable for NRIs).

- Tax payable is applicable when total income exceeds Rs 7,00,000 (not applicable for NRIs).

Additional Notes:

- Surcharge and cess will be applicable over and above the tax rates in both tax regimes.

This version provides clear distinctions between the old and new tax regimes, specifies the exemption limits based on age groups, and includes all relevant rebate and tax payable conditions.

Comparison of Tax Rates Under the New and Old Tax Regimes

|

|

|||||||

|

Age < 60 years & NRIs |

Age of 60 Years to 80 years |

Age above 80 Years |

FY 2022-23 |

FY 2023-24 |

|||

|

Up to 2,50,000 |

NIL |

NIL |

NIL |

NIL |

NIL |

||

|

₹2,50,001 - ₹3,00,000 |

5% |

NIL |

NIL |

5% |

NIL |

||

|

₹3,00,001 - ₹5,00,000 |

5% |

5% |

NIL |

5% |

5% |

||

|

₹5,00,001 - ₹6,00,000 |

20% |

20% |

20% |

10% |

5% |

||

|

₹6,00,001 - ₹7,50,000 |

20% |

20% |

20% |

10% |

10% |

||

|

₹7,50,001 - ₹9,00,000 |

20% |

20% |

20% |

15% |

15% |

||

|

₹9,00,001 - ₹10,00,000 |

20% |

20% |

20% |

15% |

15% |

||

|

₹10,00,001 - ₹12,00,000 |

30% |

30% |

30% |

20% |

15% |

||

|

₹12,00,001 - ₹12,50,000 |

30% |

30% |

30% |

20% |

20% |

||

|

₹12,50,001 - ₹15,00,000 |

30% |

30% |

30% |

25% |

20% |

||

|

₹15,00,000 and above |

30% |

30% |

30% |

30% |

30% |

||

Income Tax Slab Rates For FY 2022-23 (AY 2023-24)

a. New Tax regime until 31st March 2023

A tax rebate of up to Rs.12,500 is applicable if the total income does not exceed Rs 5,00,000 (not applicable to NRIs).

|

Income Slabs |

Individuals (for all age categories) |

|

Up to Rs 2,50,000 |

Nil |

|

Rs 2,50,001 - Rs 5,00,000* |

5% |

|

Rs 5,00,001 - Rs 7,50,000 |

10% |

|

Rs 7,50,001 - Rs 10,00,000 |

15% |

|

Rs 10,00,001 - Rs 12,50,000 |

20% |

|

Rs 12,50,001 - Rs 15,00,000 |

25% |

|

Rs 15,00,001 and above |

30% |

For the upcoming tax filing season, refer to the rates shown in the graphic above for FY 2023-24 (AY 2024-25).

b. The old tax regime

Income tax slabs for individuals under the age of 60 and HUF

|

Income Slabs |

Individuals of Age < 60 Years and NRIs |

|

Up to Rs 2,50,000 |

NIL |

|

Rs 2,50,001 - Rs 5,00,000 |

5% |

|

Rs 5,00,001 to Rs 10,00,000 |

20% |

|

Rs 10,00,001 and above |

30% |

Note:

- Individuals, HUFs under the age of 60, and NRIs can claim an income tax exemption of up to Rs 2,50,000.

- Surcharges and cesses will apply.

Income tax slab for individuals aged 60 to 80 years.

|

Income Slabs |

Individuals of Age 60 Years to 80 Years |

|

Up to Rs 3,00,000 |

NIL |

|

Rs 3,00,001 - Rs 5,00,000 |

5% |

|

Rs 5,00,001 to Rs 10,00,000 |

20% |

|

Rs 10,00,001 and above |

30% |

NOTE:

- The income tax exemption limit is up to Rs.3 lakh for senior citizens aged above 60 years but less than 80 years.

- Surcharge and cess will be applicable

Income tax slab for Individuals aged more than 80 years

|

Income Slabs |

Individuals of Age above 80 Years |

|

Up to Rs 5,00,000 |

NIL |

|

Rs 5,00,001 to Rs 10,00,000 |

20% |

|

Rs 10,00,001 and above |

30% |

NOTE:

- Income tax exemption limit is up to Rs 5 lakh for super senior citizens aged above 80 years.

- Surcharge and cess will be applicable

Revised Income Tax Slab Rate AY 2024-25 (FY 2023-24)—For New Regime

|

Income Slabs |

Income Tax Rates |

|

Up to Rs 3,00,000 |

Nil |

|

Rs 3,00,000 to Rs 6,00,000 |

5% on income which exceeds Rs 3,00,000 |

|

Rs 6,00,000 to Rs 900,000 |

Rs. 15,000 + 10% on income more than Rs 6,00,000 |

|

Rs 9,00,000 to Rs 12,00,000 |

Rs. 45,000 + 15% on income more than Rs 9,00,000 |

|

Rs 12,00,000 to Rs 1500,000 |

Rs. 90,000 + 20% on income more than Rs 12,00,000 |

|

Above Rs 15,00,000 |

Rs. 150,000 + 30% on income more than Rs 15,00,000 |

What are the major procedural changes in filing income tax returns from FY 2022-23 to FY 2023-24?

- For FY 2022-23, the default regime was the Old tax regime; if you wanted to switch to the New tax regime, you needed to complete Form 10-IE. After the due date, you must file under the previous regime exclusively.

- For FY 2023-24, the default regime shifted to the new tax regime; therefore, if you want to submit a return under the previous tax regime, claiming all deductions, exemptions, and losses, you must file Form 10-IEA by the due date. After the due date, you must file under the new system, which includes giving up the majority of your deductions and exemptions, as well as all losses.

How Do I Calculate Income Tax from Income Tax Slabs?

Illustration #1: Rohit's total taxable income is Rs 8,00,000. This income was estimated by combining all sources of income, including salary, rental income, and interest income. Deductions under Section 80 have also been lowered. Rohit would like to know his tax obligations under the previous regime for fiscal year 2023-24 (AY 2024-2025).

|

Income Tax Slabs |

Tax Rate |

Tax Amount |

|

*Income up to Rs 2,50,000 |

No tax |

- |

|

Income from Rs 2,50,000 – Rs 5,00,000 |

5% (Rs 5,00,000 – Rs 2,50,000) |

Rs 12,500 |

|

Income from Rs 5,00,000 – 10,00,000 |

20% (Rs 8,00,000 – Rs 5,00,000) |

Rs 60,000 |

|

Income more than Rs 10,00,000 |

30% |

- |

|

Tax |

|

Rs 72,500 |

|

Cess |

4% of Rs 72,500 |

Rs 2,900 |

|

Total tax in FY 2023-24 (AY 2024-25) |

Rs 75,400 |

|

Note:

Please keep in mind that Rohit is an individual taxpayer who is entitled to an income tax exemption of Rs 2,50,000. Other taxpayer assessees, i.e. elderly persons and super senior citizens, have an income-tax exemption limit of Rs 3,00,000 and Rs 5,00,000, respectively.

Individuals with a net taxable income of less than or equal to Rs 5 lakh will be eligible for a tax rebate under Section 87A under the former tax regime, which means their tax due will be zero.

Important Points to Consider If You Choose the New Tax Regime:

Please keep in mind that the tax rates under the new regime are the same for all types of individuals, including individuals, senior citizens, and super senior citizens.

Individuals with a net taxable income of less than or equal to Rs 7 lakh will be eligible for a tax rebate under Section 87A, which means their tax burden will be zero under the new regime.

What is a surcharge, and what are the applicable rates?

If your income surpasses a specific amount, you must pay additional taxes on top of your current tax rate. This is an additional tax on high-income earners.

The surcharge rates are as follows.

Income tax is 10% if total income exceeds Rs.50 lakh but less than Rs.1 crore.

If your total income exceeds Rs.1 crore but is less than Rs.2 crore, you are subject to a 15% income tax.

If your total income is more than Rs.2 crore but less than Rs.5 crore, you would be taxed at 25%.

37% income tax if total income exceeds Rs. 5 crore.

- Surcharge rates of 25% or 37% will not apply to income from dividends and capital gains taxable under sections 111A (Short Term Capital Gain on Shares), 112A (Long Term Capital Gain on Shares), and 115AD (Tax on Foreign Institutional Investors' Income). As a result, the greatest tax surcharge rate applicable to such incomes will be 15%.

- The surcharge rate for an Association of Persons (AOP) made up exclusively of businesses will similarly be limited to 15%.

The additional Health and Education cess of 4% will be added to the income tax liability.

Consequences of not filing the return by the due date for AY 2024-25

Failure to file the return before the due date for FY 2023-24 forces the taxpayer to opt for concessional rates in the New Tax regime while foregoing certain exemptions and deductions available in the present old tax system.

There are a total of 70 deductions and exemptions that are not authorized, with the most regularly utilized ones listed below:

|

Particulars |

Old Tax Regime |

New Tax regime (until 31st March 2023) |

New Tax Regime (From 1st April 2023) |

|

Income level for rebate eligibility |

₹ 5 lakhs |

₹ 5 lakhs |

₹ 7 lakhs |

|

Standard Deduction |

₹ 50,000 |

– |

₹ 50,000 |

|

Effective Tax-Free Salary income |

₹ 5.5 lakhs |

₹ 5 lakhs |

₹ 7.5 lakhs |

|

Rebate u/s 87A |

12,500 |

12,500 |

25,000 |

|

HRA Exemption |

✓ |

X |

X |

|

Leave Travel Allowance (LTA) |

✓ |

X |

X |

|

Other allowances including food allowance of Rs 50/meal subject to 2 meals a day |

✓ |

X |

X |

|

Entertainment Allowance Deduction and Professional Tax |

✓ |

X |

X |

|

Perquisites for official purposes |

✓ |

✓ |

✓ |

|

Interest on Home Loan u/s 24b on self-occupied or vacant property |

✓ |

X |

X |

|

Interest on Home Loan u/s 24b on let-out property |

✓ |

✓ |

✓ |

|

Deduction u/s 80C (EPF|LIC|ELSS|PPF|FD|Children’s tuition fee etc) |

✓ |

X |

X |

|

Employee’s (own) contribution to NPS |

✓ |

X |

X |

|

Employer’s contribution to NPS |

✓ |

✓ |

✓ |

|

Medical insurance premium – 80D |

✓ |

X |

X |

|

Disabled Individual – 80U |

✓ |

X |

X |

|

Interest on education loan – 80E |

✓ |

X |

X |

|

Interest on Electric vehicle loan – 80EEB |

✓ |

X |

X |

|

Donation to Political party/trust etc – 80G |

✓ |

X |

X |

|

Savings Bank Interest u/s 80TTA and 80TTB |

✓ |

X |

X |

|

Other Chapter VI-A deductions |

✓ |

X |

X |

|

All contributions to Agniveer Corpus Fund – 80CCH |

✓ |

Did not exist |

✓ |

|

Deduction on Family Pension Income |

✓ |

X |

✓ |

|

Gifts up to Rs 50,000 |

✓ |

✓ |

✓ |

|

Exemption on voluntary retirement 10(10C) |

✓ |

✓ |

✓ |

|

Exemption on gratuity u/s 10(10) |

✓ |

✓ |

✓ |

|

Exemption on Leave encashment u/s 10(10AA) |

✓ |

✓ |

✓ |

|

Daily Allowance |

✓ |

✓ |

✓ |

|

Transport Allowance for a specially-abled person |

✓ |

✓ |

✓ |

|

Conveyance Allowance |

✓ |

✓ |

✓ |

Comparison of Income Tax Slabs Under the New Regime Before and After Budget

Only the income tax slabs for the new regimes were altered in the Union Budget 2023.

|

Slab |

New Tax Regime FY 2022-23 (AY 2023-24) |

New Tax Regime FY 2023-24 (AY 2024-25) |

|

₹0 - ₹2,50,000 |

– |

– |

|

₹2,50,000 - ₹3,00,000 |

5% |

– |

|

₹3,00,000 - ₹5,00,000 |

5% |

5% |

|

₹5,00,000 - ₹6,00,000 |

10% |

5% |

|

₹6,00,000 - ₹7,50,000 |

10% |

10% |

|

₹7,50,000 - ₹9,00,000 |

15% |

10% |

|

₹9,00,000 - ₹10,00,000 |

15% |

15% |

|

₹10,00,000 - ₹12,00,000 |

20% |

15% |

|

₹12,00,000 - ₹12,50,000 |

20% |

20% |

|

₹12,50,000 - ₹15,00,000 |

25% |

20% |

|

>₹15,00,000 |

30% |

30% |

Old vs. new tax regime? Which one is better?

The new tax structure will mostly help middle-class taxpayers with taxable incomes of up to Rs 15 lakh. High-income earners would benefit more from the previous regime.

The new income tax scheme is helpful to those who make little investments. Because the new system has six lower-income tax brackets, everyone who pays taxes without claiming tax deductions can benefit from paying a reduced tax rate under the new regime. For example, an assessee with a total income before deduction of up to Rs 12 lakh will have a larger tax due under the old system if their investments are less than Rs 3,12,500. Therefore, if you invest less in tax-saving plans, choose the New Tax Regime

That being said, if you already have a financial plan in place for wealth creation, such as investing in tax-saving instruments, filing medical claims and life insurance, paying for children's tuition, paying EMIs on education loans, purchasing a home with a home loan, and so on, the old regime benefits you with higher tax deductions and lower tax outgo.

Given the foregoing and the new income tax regime, taxpayers who wish to take advantage of the lower tax rates may compare both regimes. As a result, it is best to do a comparative examination and study of both regimes before deciding on the most advantageous one, as this may differ from person to person.

When Can I Choose the Old or New Regime?

|

Nature of Income |

Time of Selection of option of old vs new regime |

|

Income from Salary or any other head of income attracting TDS |

At the start of the financial year, an employee has the choice to select the tax regime and inform their employer, whereas the default regime shall be a new tax regime. It cannot be modified during the year. However, the option can be modified when filing the Income Tax Return. |

|

Income from Business & Profession |

In case you have Business or professional income, the choice between tax regimes can only be made once in a lifetime. |

Income Tax Rate for Domestic Companies, FY 2023-24

|

Particulars |

Old regime Tax rates |

New Regime Tax rates |

|

Company opts for section 115 BAB (not covered in sections 115BA and 115BAA) & is registered on or after October 1, 2019, and has commenced manufacturing on or before 31st March 2024 and subject to the conditions specified in the section. Applicable from AY 2020-21 and onwards. |

– |

15% |

|

Company opts for Section 115 BAA, wherein the total income of a company has been calculated without claiming specified deductions, incentives, or exemptions and additional depreciation as specified in the section. Applicable from AY 2020-21 and onwards. |

– |

22% |

|

The company opts for section 115BA registered on or after March 1, 2016 and engaged in the manufacture of any article or thing and does not claim the deduction as specified in the section. Applicable from AY 2017-18 and onwards. |

– |

25% |

|

Turnover or gross receipt of the company is less than Rs. 400 crore in the previous year 2020-21 |

25% |

25% |

|

Any other domestic company |

30% |

30% |

Please see the new sections to determine the applicability of the aforesaid concessional income tax rates.

NOTE:

- In all situations, an additional 4% Health and Education cess will be levied on the income tax.

- The surcharge for firms is as below

- Income tax rates are as follows: 7% for total income over Rs 1 crore, 12% for total income over Rs 10 crore, and 10% for domestic companies that use sections 115BAA and 115BAB.

Income Tax Rate for Partnership Firm or LLP under the Old/New Regime

A partnership firm or LLP is taxed at 30%.

NOTE:

A 12% surcharge is paid on income of more than Rs 1 crore.

A 4% health and education levy will apply.

The upcoming tax regime will not include any concessional rates for companies or LLPs.

Income tax slab rates for FY 2019-20, FY 2020-21, FY 2021-22 and FY 2022-23

Income tax slab for individuals under the age of 60 and HUF

|

Income Tax Slab |

Tax Rates for Individual & HUF Below the Age Of 60 Years & NRIs |

|

Up to ₹2,50,000* |

Nil |

|

₹2,50,001 to ₹5,00,000 |

5% |

|

₹5,00,001 to ₹10,00,000 |

20% |

|

Above ₹10,00,000 |

30% |

NOTE:

- Individuals, HUFs under the age of 60, and NRIs can claim an income tax exemption of up to Rs 2,50,000.

- Surcharges and cess will be applicable, as described above.

- An additional 4% health and education cess will be applicable on the tax and surcharge amount.

Income tax slab for Individual aged above 60 years to 80 years

Income Tax Slab

Tax Rates for Senior citizens aged above 60 Years & Less than 80 Years

Up to ₹ 3,00,000*

No tax

₹3,00,000 - ₹5,00,000

5%

₹5,00,000 - ₹10,00,000

20%

More than ₹10,00,000

30%

NOTE:

- Senior adults aged 60 and over are eligible for an income tax exemption of up to Rs. 3 lakh.

- Surcharges and cess will be applicable, as described above.

Income tax slab for Individual aged more than 80 years

|

Income Tax Slab |

Tax Rates for Super Senior Citizens (Aged 80 Years And Above) |

|

Up to ₹5,00,000* |

No tax |

|

₹5,00,000 - ₹10,00,000 |

20% |

|

More than ₹10,00,000 |

30% |

NOTE:

- Income tax exemption limit is up to Rs 5 lakh for super senior citizens aged above 80 years.

- Surcharge and cess will be applicable as discussed above

Income Tax Slabs for Domestic Companies in Fiscal Years 2019-20, 2020-21, 2021-22, and 2022-23

|

Turnover Particulars |

Tax Rate |

|

Gross turnover up to 250 Cr. in the previous year |

25% |

|

Gross turnover exceeding 250 Cr. in the previous year |

30% |

NOTE:

In addition, the following taxes and surcharges are levied:

- Cess: 4% of corporation taxes.

- Surcharge is applicable when taxable income exceeds 1 crore but falls below 10 crores. 7%

- Taxable income exceeds 10 crores: 12%

FY 2018-19: Income Tax Slab Rates

Income tax slab for Individual aged below 60 years & HUF

|

Income Tax Slab |

Tax Rates for Individual & HUF Below the Age Of 60 Years |

|

Income up to Rs 2,50,000* |

No tax |

|

Income from Rs 2,50,000 – Rs 5,00,000 |

5% |

|

Income from Rs 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs 10,00,000 |

30% |

NOTE:

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above.

- Surcharge applicability:

- 10% of income tax, where total income exceeds Rs.50 lakh up to Rs.1 crore.

- 15% of income tax, where the total income exceeds Rs.1 crore.

Income tax slab for Individuals aged above 60 years to 80 years

|

Income Tax Slab |

Tax Rate for Senior citizens aged 60 Years But Less than 80 Years |

|

Income up to Rs 3,00,000* |

No tax |

|

Income from Rs 3,00,000 - Rs 5,00,000 |

5% |

|

Income from Rs 5,00,000 - 10,00,000 |

20% |

|

Income more than Rs 10,00,000 |

30% |

NOTE:

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above.

- Surcharge applicability:

- 10% of income tax, where total income exceeds Rs.50 lakh up to Rs.1 crore.

- 15% of income tax, where the total income exceeds Rs.1 crore.

Income tax slab for Individuals aged more than 80 years

|

Income Tax Slab |

Tax Rates for Super Senior Citizens (Aged 80 Years And Above) |

|

Income up to Rs 5,00,000* |

No tax |

|

Income from Rs 5,00,000 - Rs 10,00,000 |

20% |

|

Income more than Rs 10,00,000 |

30% |

NOTE:

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above.

- Surcharge applicability:

- 10% of income tax, where total income exceeds Rs.50 lakh up to Rs.1 crore.

- 5% of income tax, where the total income exceeds Rs.1 crore

Income Tax Slab for Domestic Companies FY 2018-19

|

Turnover Particulars |

Tax Rate |

|

Gross turnover upto 250 Crore in the previous year |

25% |

|

Gross turnover exceeding 250 Crore in the previous year |

30% |

NOTE:

- In addition cess and surcharge is levied as follows:

- Cess: 4% of corporate tax.

- Surcharge applicability:

- Taxable income is more than 1 Crore but less than 10 Crore: 7%

- Taxable income is more than 10 Crore :12%

FY 2017-18: Income Tax Slab Rates

Income tax slab for Individual below 60 years & HUF

|

Income Tax Slab |

Tax Rates for Individual & HUF Below the Age Of 60 Years |

|

Income up to Rs 2,50,000* |

No tax |

|

Income from Rs 2,50,000 – Rs 5,00,000 |

5% |

|

Income from Rs 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs 10,00,000 |

30% |

NOTE:

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above

- Surcharge applicability:

- 10% of income tax, where total income exceeds Rs. 50 lakh up to Rs. 1 crore.

- 15% of income tax, where the total income exceeds Rs. 1 crore.

Income tax slab for Individual aged above 60 years to 80 years

|

Income Tax Slab |

Tax Rate for Senior citizens aged 60 Years But Less than 80 Years |

|

Income up to Rs 3,00,000* |

No tax |

|

Income from Rs 3,00,000 – Rs 5,00,000 |

5% |

|

Income from Rs 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs 10,00,000 |

30% |

NOTE:

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above

- Surcharge applicability:

- 10% of income tax, where total income exceeds Rs.50 lakh up to Rs.1 crore

- 15% of income tax, where the total income exceeds Rs.1 crore.

Income tax slab for Individual aged more than 80 years

|

Income Tax Slab |

Tax Rates for Super Senior Citizens (Aged 80 Years And Above) |

|

Income up to Rs 5,00,000* |

No tax |

|

Income from Rs 5,00,000 – 10,00,000 |

20% |

|

Income more than Rs 10,00,000 |

30% |

NOTE:

- An additional 4% Health & education cess will be applicable on the tax amount calculated as above

- Surcharge applicability:

- 10% of income tax, where total income exceeds Rs.50 lakh up to Rs.1 crore

- 15% of income tax, where the total income exceeds Rs.1 crore.

Income Tax Slab for Domestic Companies FY 2017-18

|

Turnover Particulars |

Tax Rate |

|

Gross turnover upto 250 Cr. in the previous year |

25% |

|

Gross turnover exceeding 250 Cr. in the previous year |

30% |

NOTE:

- In addition cess and surcharge is levied as follows: Cess: 4% of corporate tax.

- Surcharge applicability:

- Taxable income is more than 1 Crore but less than 10 Crore: 7%

- Taxable income is more than 10 Crore: 12%

Don’t fall behind your taxes!

With Taxring , get your taxes done early and enjoy peace of mind.

Frequently Asked Questions

Q1.How should I calculate income tax for FY 2023-24?

For FY 2023-2024, taxpayers have the option to select between two tax regimes: the old tax regime or the new one. The income tax should be calculated by using the applicable slab rates.

Q2.Can I claim 80C deductions and opt for a new income tax slab regime?

No, the new tax regime does not allow many deductions and exemptions which are otherwise available in the old tax regime. Deductions u/s 80C cannot be claimed if the taxpayer is opting for a New tax regime

Q3.How does the government collect the taxes?

Taxes are collected by the Government through three means:

- Voluntary payment by taxpayers through various designated Banks. For example, Advance Tax and Self Assessment Tax payments,

- Taxes deducted at source [TDS] and

- Taxes collected at source [TCS].

Q3.Are there separate slab rates for different categories?

Yes, there are separate slab rates under the old tax regimes. However under the new tax regimes, there are no categories as such.

Do I need to file an Income Tax Return (ITR) if my annual income is below ₹3 lakh of the basic exemption limit?

Even if your income is below the exemption limit, you must file your ITR if any of these conditions apply to you.

Q3.Is the due date for filing an income tax return the same for all taxpayers?

No, the due date for all the taxpayers is not the same. For individual taxpayers for whom tax audit is not applicable, the due date is 31st July of the assessment year unless extended by the government.

Q4.What is the meaning of rebate under section 87A under the IT Act?

Section 87A is a legal provision which allows for tax rebates under the Income Tax Act of 1961. The section, which was inserted through the Finance Act of 2013, provides tax relief for individuals earning below a specified limit. Section 87 A provides that anyone who is residing in India and whose income does not exceed Rs 5,00,000 is eligible to claim a rebate. Thus full income tax rebate is available to individuals with less than Rs 5 Lakh of total taxable income under the old regime, whereas under the new tax regime, the income limit is Rs. 7,00,000. This rebate is applicable only to individuals and not companies, etc and is calculated before adding the health and educational cess of 4 %.

Q5.Who decides the IT slab rates, and can they change?

Yes, IT slab rates can be changed by the government. If there are changes in IT slab rates for the financial year, then they are introduced in the Budget and presented in Parliament.

Q6.What is the Previous year and Assessment year?

The Income-tax law has two important terms: (i) Previous year and (ii) Assessment year. It is extremely important for determining the taxpayer's income and tax payable amount.

(i) Previous year: The previous year is the year in which the income is earned which typically starts on 1st April and ends on 31st March. Whereas, the year immediately following the previous year (1st April to 31st March) is known as ‘Assessment Year’.

For example, the current previous year is from 1st April 2023 to 31st March 2024, i.e. FY 2023-24. The corresponding assessment year is 1st April 2024 to 31st March 2025, i.e. AY 2024-25.

Q7.How to file an income tax return online?

To submit your income tax return online, log on to either the income tax e-filing portal or you can also e-file through Taxring. For e-filing through the income tax portal, log in to www.incometax.gov.in. You can also download the offline JSON utility and file the ITR. Remember to verify the return within 30 days of filing the ITR. ITR filing is incomplete without verification, failure to verify the return will be deemed that you have not filed the return at all.

Please click here to read the step-by-step guide on how to e-file ITR on the income tax e-filing portal.

Q.How much income is tax free in India?

Income tax law has prescribed a basic exemption limit for individuals up to which the taxpayers are not required to pay taxes. Such a limit is different for different categories of taxpayers under the old tax regime. Individuals below 60 years of age are not required to pay tax upto the income limit of Rs 2.5 Lakh. Individuals above 60 years but less than 80 years of age are not required to pay tax upto Rs 3 lakh of income. Individuals above 80 years are not required to pay tax upto Rs 5 lakh of income. The basic exemption limit for all the individuals under the new tax regime is Rs 3 lakh, irrespective of age.

Q.How to calculate surcharge on income tax?

The surcharge is a tax on tax. Hence surcharge is calculated on the tax payable and not on the income earned. For example, if you have an income of Rs 1000 with 30% tax of Rs. 300, if the income is subject to surcharge then 10% surcharge would be levied on tax of Rs. 300 i.e. Rs 30. Surcharge is levied at different rates i.e

- 10% is levied is total income is > 50 lakh,

- 15% is levied if total income is more than 1 crore,

- 25% of income if total income is > 2 crores.

Q.How to calculate the age of a senior citizen for income tax?

Individual above the age of 60 years is regarded as a senior citizen whereas an individual above 80 years is regarded as a super senior citizen for the purpose of income tax. Senior citizens and super senior citizens have been provided higher tax exemption limits and specific benefits by the income tax law in order to provide some relief.

Q.How to pay income tax online?

The income tax payment facility has been migrated from OLTAS to the 'e-Pay Tax' facility of the e-filing portal. You can refer to this step-by-step guide for making your tax payments.

Q.Will my income be taxed if I am an agriculturist?

Any income which is generated from agriculture or its allied activities will not be taxed. However, it will be considered for determining the tax rate while calculating tax on any non-agricultural income that you may have.

Q.If my income is 5 lakh, how much tax do I have to pay?

No tax is payable since tax rebate is available upto Rs. 5 lakh under old regime and Rs. 7 lakh under new regime.

If my income is 7 lakh, how much tax do I have to pay?

No tax is payable under the new tax regime up to Rs. 7 lakh.

If my income is 10 lakh, how much tax do I have to pay?

New Regime: 62,400

Old Regime: 1,17,000

Q.If my income is 15 lakh, how much tax do I have to pay?

New Regime: 1,56,000

Old Regime: 2,73,000

Q.If my income is 20 lakh, how much tax do I have to pay?

New Regime: 3,12,000

Old Regime: 4,29,000

These taxes have been calculated based on the assumption that they are Net Taxable Income after deducting all deductions. However, you may add your exact income details on this simplified income tax calculator to find out the exact tax payable. If you are calculating for FY 2023-24, make sure to select the correct financial year.

Q.Do I have to mandatorily opt for a New tax regime while filing returns for AY 2024-25?

Taxpayers have the freedom to select the tax regimes, if one needs to opt for the old regime and claim deductions, exemptions, and losses must file their income tax returns by opting out of the new regime.

For employees, the choice needs to be made at the beginning of the year and can be modified at the time of ITR filing. However, if you are engaged in business or profession, the option to switch to the Old Tax regime is available only once in your lifetime. We recommend that you carefully evaluate your tax outgo under both regimes and then select the one which is most beneficial to you.

Q What is e-verification of Income tax returns? How to do it?

The income tax return needs to be verified post submission. It is applicable for all types of return original, belated, revised or updated return. It is mandatory to verify the return within 30 days from the date of filing. Failure to verify the return will be deemed that you have not filed the return at all. One can do the verification either by physically by appending the signature on the ITR acknowledgement form (ITR V) manually and sending it to CPC, Bengaluru by courier or post OR electronically via Aadhaar OTP or EVC (electronic verification code) or Digital signature during or after the submission of Income tax return.

Q,Is standard deduction applicable in the new tax regime?

Yes, the standard deduction is allowed under the new tax regime for FY 2023-24. However, it was not allowed as a deduction for FY 2022-23.

What deductions are allowed in the new tax regime?

One can claim a few selective deductions under the new tax regime for FY 2023-24, such as a standard deduction of Rs.50,000, interest on Home Loan u/s 24b on let-out property, employer’s contribution to NPS u/s 80CCD, Contributions to Agniveer Corpus Fund u/s 80CCH, Deduction on Family Pension Income (lower of 1/3rd of actual pension or 15,000).

Is HRA exemption available in the new tax regime?

No, HRA exemption u/s10(13A) is not allowed in the new tax regime. Along with that most claimed exemptions are also NOT allowed such as Leave Travel Allowance (LTA), Exemption on voluntary retirement 10(10C), Exemption on gratuity u/s 10(10), Exemption on Leave encashment u/s 10(10AA), Daily Allowance, Transport Allowance for a specially-abled person, Conveyance Allowance etc,

How to choose the tax regimes while filing?

There are differential processes to opt in for tax regimes between FY 2022-23 and FY 2023-24.

For 2022-23 - default regime is old tax regime

If the total income does not include profit and gains from business & profession and new tax regime needs to be opted, then one must file Form 10IE (online form from Income Tax portal) before the submission of income tax return by clicking Yes for “Do you opt for sec 115 BAC(1)?”, else one must file income tax return only without the requirement to file Form 10IE. In both the scenarios return must be submitted within the due date.

For 2023-24 - default regime is new tax regime

If the total income does not include profit and gains from business & profession and new old regime needs to be opted, then one must file Form 10 IEA (online form from Income Tax portal) before the submission of income tax return by clicking Yes for “Do you opt out from sec 115 BAC(1A)?”, else one must file income tax return only without the requirement to file Form 10 IEA. In both the scenarios return must be submitted within the due date.

Q.Which form has to be filed for opting the old tax regime?

Form 10-IEA must be filed before the due date for opting to pay taxes under the old tax regime.

Q.What happens if an individual doesn’t submit the Form 10-IEA timely?

If an individual forgets to complete the submission of Form 10-IEA before or during the filming of the ITR, they will be unable to choose the old tax regime. The delayed submission of the form of failure to submit means that the income tax department will compute tax as per the new tax regime.

Related articles:

New tax Regime vs Old tax Regime ?

ITR Filing Last date For FY 2023 -24

http://How to file ITR Online yourself ?

How to File ITR Through CA/Tax expert & Chargese?

What are the ITR Filing Pricing plan for individual &Business , Proffessionals ?