Get the latest update on the New tax regime

The government has introduced a new tax regime, which is now the default regime for filing income tax returns. It's essential to understand the changes and compare the tax liability under both the new and old tax regimes before filing your return.

Under the new tax regime, individuals with an annual income of up to Rs 7 lakh will not be eligible for certain deductions. These deductions, which are available under the old tax regime, include:

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Deductions under Section 80C, 80D, 80U, 80E, 80G, 80TTA, 80TTB, and other Chapter VI A deductions.

Key Changes:

- The new tax regime offers a simplified tax structure with lower tax rates.

- No income tax is payable up to Rs 7,00,000.

- Senior citizens' exemption limit has been increased to Rs 7,00,000.

Key Differences:

Old Tax Regime:

- Basic exemption limit for senior citizens: Rs 3,00,000

- Basic exemption limit for super senior citizens: Rs 5,00,000

New Tax Regime:

- No income tax payable up to Rs 7,00,000

- Lower tax rates (10% to 30% tax slab)

- No deductions for HRA, LTA, and other allowances

- Limited exemptions

- Simplified tax structure, but reduced tax benefits

Implications for You:

- Reduced tax liability, but reduced deductions

- Need to reassess your tax planning strategy

- Consider consulting a tax expert to optimize your tax savings

Our Expertise:

- Personalized tax guidance

- Maximize your tax savings

- Expert analysis of your tax situation

What's Not Available in the New Tax Regime:

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Deductions under Section 80C, 80D, 80U, 80E, 80G, 80TTA, 80TTB, and other Chapter VI A deductions.

Compare Your Tax Liability:

Before filing your return, calculate your tax liability under both regimes to determine which one benefits you more. Our experts can help you with this comparison and ensure you make the most of the new tax regime.

It is important to note that the old tax regime will still be applicable to individuals who opt for it. However, the new tax regime offers a simpler tax structure with lower tax rates, but with limited deductions and exemptions. Individuals must carefully consider their financial situation and tax planning strategies before opting for either regime.

Old vs New Tax Regime: Which Is Better New Or Old Tax Regime For Salaried Employees?

The Budget 2023 produced significant confusion among taxpayers over the choice between the old and new tax regimes. The government included a number of incentives in the 2023 Budget to stimulate the implementation of the new system.

These developments indicate that the administration aims to shift taxpayers to the new system and eventually phase out the old one. Even if the new regime is now the default tax regime, the old regime will continue to exist.

Interim Budget 2024-2025 Updates:

No changes were made in direct taxes in the Interim Budget 2024-2025

New Tax Regime

Budget 2020 featured a new tax framework that adjusted tax slabs and provided taxpayers with concessional tax rates. However, people who choose the new regime will be unable to claim a number of exemptions and deductions, including HRA, LTA, 80C, 80D, and others. As a result, the new tax regime failed to gain traction. To urge taxpayers to adopt the new regime, the government adopted five important modifications in Budget 2023, which will remain unchanged for Fiscal Year 2024-2025 because no changes were made in the Interim Budget 2024. They are:

Higher Tax Rebate Limit: - A full tax rebate on income up to ₹7 lakhs has been established. Under the prior tax regime, the threshold was ₹5 lakhs. The new tax regime exempts taxpayers with incomes up to ₹7 lakhs from paying any taxes.

Streamlined tax slabs: The tax exemption ceiling has been raised to ₹3 lakhs. The new tax slabs are:

|

Total Income |

Rate of Tax |

|

up to ₹3,00,000 |

Nil |

|

₹3,00,001- ₹6,00,000 |

5% |

|

₹6,00,001- ₹9,00,000 |

10% |

|

₹9,00,001- ₹12,00,000 |

15% |

|

₹12,00,001- ₹15,00,000 |

20% |

|

₹15,00,001 and above |

30% |

Tax rates in both regimes are compared as follows:

|

Income Slab |

Old Tax Regime |

New tax Regime |

New Tax Regime |

|

₹0 - ₹2,50,000 |

- |

- |

- |

|

₹2,50,000 - ₹3,00,000 |

5% |

5% |

- |

|

₹3,00,000 - ₹5,00,000 |

5% |

5% |

5% |

|

₹5,00,000 - ₹6,00,000 |

20% |

10% |

5% |

|

₹6,00,000 - ₹7,50,000 |

20% |

10% |

10% |

|

₹7,50,000 - ₹9,00,000 |

20% |

15% |

10% |

|

₹9,00,000 - ₹10,00,000 |

20% |

15% |

15% |

|

₹10,00,000 - ₹12,00,000 |

30% |

20% |

15% |

|

₹12,00,000 - ₹12,50,000 |

30% |

20% |

20% |

|

₹12,50,000 - ₹15,00,000 |

30% |

25% |

20% |

|

>₹15,00,000 |

30% |

30% |

30% |

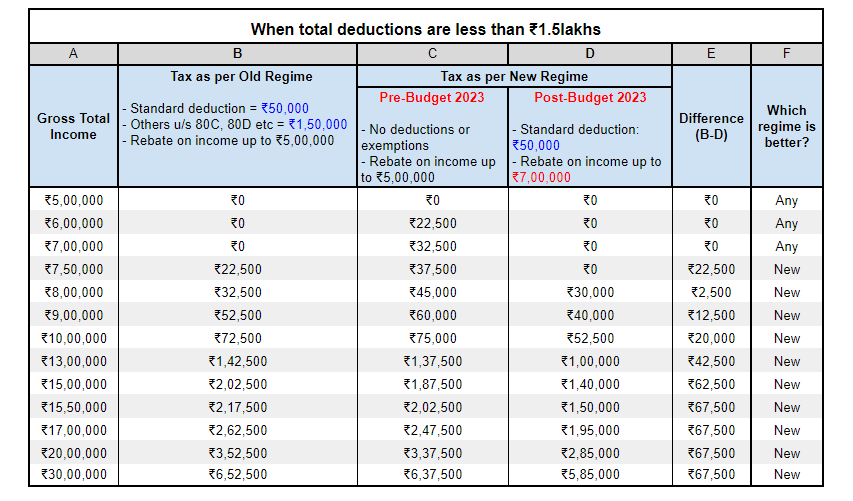

1. Standard Deduction and Family Pension Benefits:

- Standard Deduction:Previously exclusive to the old tax regime, the ₹50,000 standard deduction is now accessible under both old and new tax regimes. Coupled with applicable rebates, this elevates your tax-free income to ₹7.5 lakhs in the new regime.

- Family Pension Deduction:Those receiving family pensions can claim a deduction of ₹15,000 or 1/3rd of the pension amount, whichever is lower.

2. Reduced Surcharge for High Net Worth Individuals:

- The surcharge rate for individuals earning over ₹5 crores has been slashed from 37% to 25%, effectively lowering their tax burden from 42.74% to 39%.

3. Enhanced Leave Encashment Exemption:

- Non-government employees now benefit from a significantly increased exemption limit for leave encashment, soaring from ₹3 lakhs to ₹25 lakhs—a remarkable 8-fold increment.

4. Default Tax Regime and Annual Option: - Starting FY 2023-24, the new tax regime becomes the default choice. If preferring the old regime, taxpayers must submit their returns alongside Form 10IEA before the deadline. Annually, taxpayers may freely switch between regimes to optimize tax advantages.

Old Tax Regime

Old Tax Regime The old governance is the duty system that was previous to the perpetration of the new governance. This governance provides over 70 rejections and deductions, including HRA and LTA, that can reduce your taxable income and cut your duty payments. Section 80C is the most popular and generous deduction, allowing taxpayers to reduce their taxable income by over toRs.1.5 lakh. Taxpayers can choose between the being and new duty administrations.

Difference Between Old Vs New Tax Regime: Which is Better?

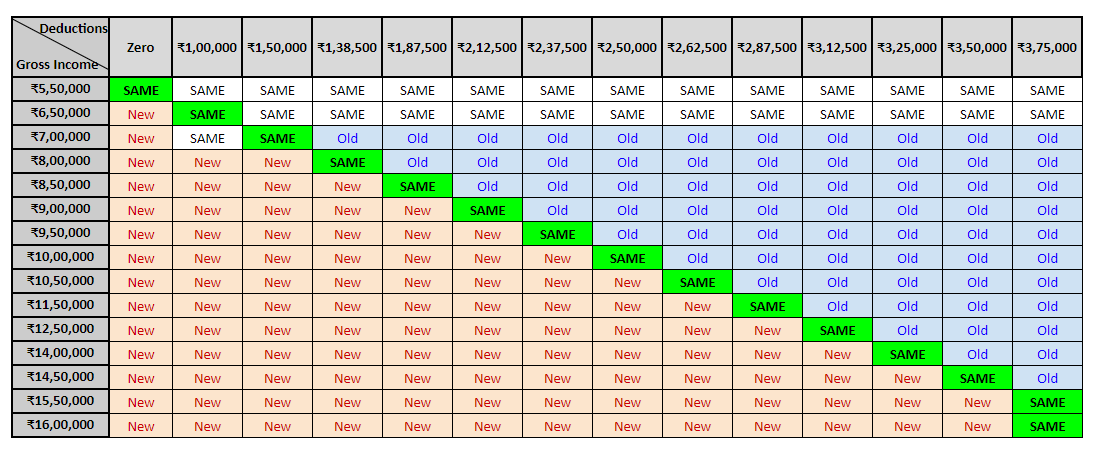

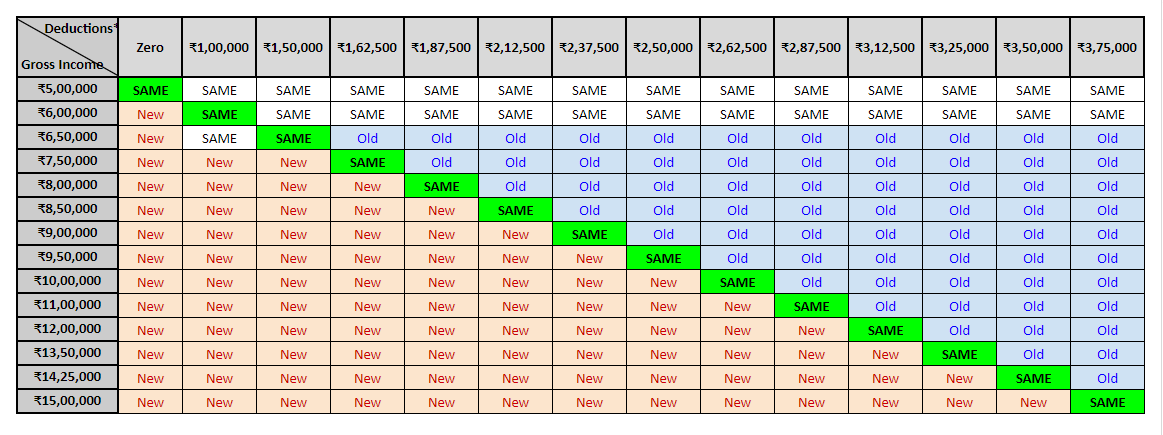

The decision to transfer to the new or continue in the old duty system, or which governance is preferable for you, will be grounded on the duty savings deductions and immunity available under the old duty governance. To make effects easier, we have estimated a breakeven point for different payment situations( see the map below) for salaried individualities under the age of 60. This can be used to elect the applicable governance.

The Breakeven Threshold for Deciding Between New and Old Tax Regimes.

The breakeven point is the amount at which the two tax regimes will have the same tax liability.

If your total qualified deductions and exemptions under the old tax regime exceed the breakeven threshold for your income level, you should stay in that regime. On the other side, if the breakeven point is higher, switching to the new tax system is more advantageous.

If you have salary income

|

Income Level |

Less: Standard Deduction |

Net Income |

Tax under both regimes |

Additional Deductions (over & above standard deduction) required in Old Regime to Break Even |

Which Regime to choose old or new tax regime |

|

7,00,000 |

50,000 |

6,50,000 |

0 |

1,50,000 |

You will benefit only in new regime |

|

8,00,000 |

50,000 |

7,50,000 |

36,400 |

1,38.500 |

Old regime: if deductions > Rs 1,38,500 New regime: if deductions < Rs 1,38,500 |

|

9,00,000 |

50,000 |

8,50,000 |

41,600 |

2,12,500 |

Old regime: if deductions > Rs 2,12,500 New regime: if deductions < Rs 2,12,500 |

|

10,00,000 |

50,000 |

9,50,000 |

54,600 |

2,50,000 |

Old regime: if deductions > Rs. 2,50,000 New regime: if deductions < Rs 2,50,000 |

|

12,50,000 |

50,000 |

₹12,00,000 |

₹93,600 |

3,12,500 |

Old regime: if deductions > Rs. 3,12,500 New regime: if deductions < Rs 3,12,500 |

|

15,50,000 |

50,000 |

₹14,50,000 |

₹1,45,600 |

₹3,58,000 |

Old regime: if deductions > Rs. 3,58,000 |

|

₹15,50,000 |

₹50,000 |

₹15,00,000 |

₹1,56,000 |

₹3,75,000 |

Old regime: if deductions > Rs. 3,75,000 New regime: if deductions < Rs 3,75,000 |

|

16,00,000 |

₹50,000 |

₹15,50,000 |

₹1,71,600 |

₹3,75,000 |

Old regime: if deductions > Rs. 3,75,000 |

If you have income other than salary:

Navigating Tax Choices: Comparing Old vs. New Regimes

Making the choice between the old and new tax regimes involves strategic consideration of your deductions:

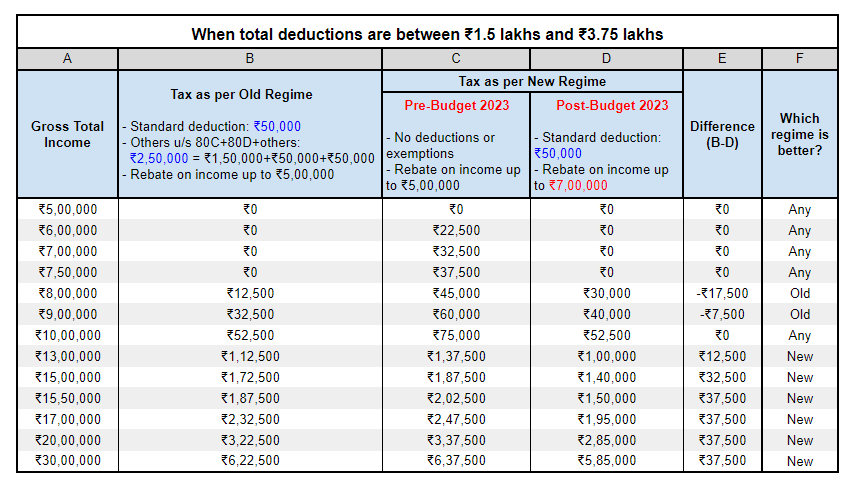

-For deductions up to ₹1.5 lakhs: Opting for the new regime typically offers greater benefits.

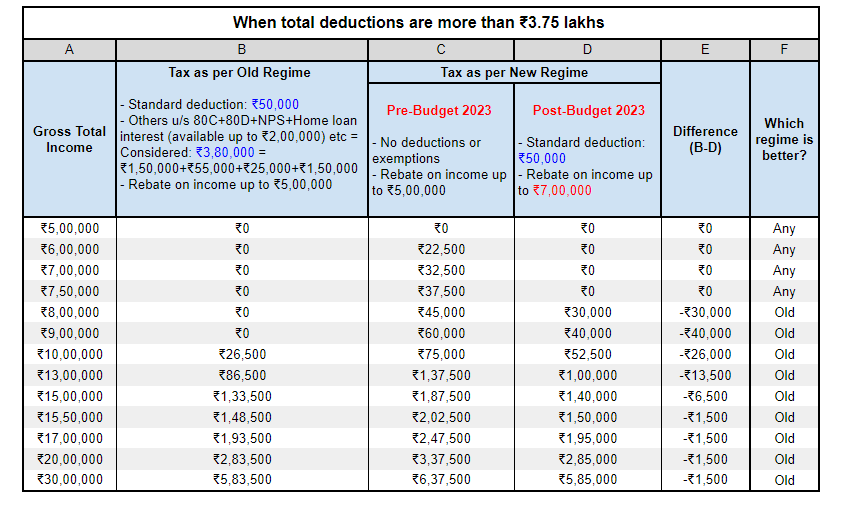

- When deductions exceed ₹3.75 lakhs: The old regime may provide more advantageous tax outcomes.

- Deductions between ₹1.5 lakhs and ₹3.75 lakhs: Your decision should be based on your specific income level and tax-saving potential.

These estimates serve as a guide to help you determine which tax regime aligns best with your financial circumstances and objectives.

The new tax structure benefits those with total deductions of ₹1.5 lakhs or less.

When total deductions exceed ₹3.75 lakhs, the former tax regime may be favorable.

When total deductions range from ₹1.5 lakh to ₹3.75 lakh: Will depend on different income levels.

What Deductions and Exemptions Are Available Under the New Tax Regime?

Here is a comparison between the deductions and exemptions available under the new and the old tax regime:

|

Particulars |

Old Tax Regime |

New tax Regime |

New Tax Regime |

|

Income level for rebate eligibility |

₹ 5 lakhs |

₹ 5 lakhs |

₹ 7 lakhs |

|

Standard Deduction |

₹ 50,000 |

- |

₹ 50,000 |

|

Effective Tax-Free Salary income |

₹ 5.5 lakhs |

₹ 5 lakhs |

₹ 7.5 lakhs |

|

Rebate u/s 87A |

₹12,500 |

₹12,500 |

₹25,000 |

|

HRA Exemption |

✓ |

X |

X |

|

Leave Travel Allowance (LTA) |

✓ |

X |

X |

|

Other allowances including food allowance of Rs 50/meal subject to 2 meals a day |

✓ |

X |

X |

|

Standard Deduction (Rs 50,000) |

✓ |

X |

✓ |

|

Entertainment Allowance and Professional Tax |

✓ |

X |

X |

|

Perquisites for official purposes |

✓ |

✓ |

✓ |

|

Interest on Home Loan u/s 24b on: Self- occupied or vacant property |

✓ |

X |

X |

|

Interest on Home Loan u/s 24b on: Let-out property |

✓ |

✓ |

✓ |

|

Deduction u/s 80C (EPF | LIC | ELSS | PPF | FD | Children's tuition fee etc) |

✓ |

X |

X |

|

Employee's (own) contribution to NPS |

✓ |

X |

X |

|

Employer's contribution to NPS |

✓ |

✓ |

✓ |

|

Medical insurance premium - 80D |

✓ |

X |

X |

|

Disabled Individual - 80U |

✓ |

X |

X |

|

Interest on education loan - 80E |

✓ |

X |

X |

|

Interest on Electric vehicle loan - 80EEB |

✓ |

X |

X |

|

Donation to Political party/trust etc - 80G |

✓ |

X |

X |

|

Savings Bank Interest u/s 80TTA and 80TTB |

✓ |

X |

X |

|

Other Chapter VI-A deductions |

✓ |

X |

X |

|

All contributions to Agniveer Corpus Fund - 80CCH |

✓ |

Did not exist |

✓ |

|

Deduction on Family Pension Income |

✓ |

X |

✓ |

|

Gifts upto Rs 50,000 |

✓ |

✓ |

✓ |

|

Exemption on voluntary retirement 10(10C) |

✓ |

✓ |

✓ |

|

Exemption on gratuity u/s 10(10) |

✓ |

✓ |

✓ |

|

Exemption on Leave encashment u/s 10(10AA) |

✓ |

✓ |

✓ |

|

Daily Allowance |

✓ |

✓ |

✓ |

|

Conveyance Allowance |

✓ |

✓ |

✓ |

|

Transport Allowance for a specially-abled person |

✓ |

✓ |

✓ |

How to Choose Between Old and New Tax Regimes?

When picking between the two tax regimes, it is critical to consider the tax breaks and deductions available under the previous tax regime. After deducting all eligible exemptions and deductions, the net taxable income can be calculated. Calculating the tax liability based on this net taxable income under the previous tax regime allows for a comparison with the tax due under the new tax regime.

Choosing the regime with the lowest tax burden is the logical option, and it is critical to notify the employer of this decision so that the appropriate Tax taken at Source (TDS) can be taken from your salary.

If you have a loss from house property, capital gains, or business and profession, you must consider them when deciding on a regime. Along with the current year's losses, the prior year's losses that were eligible for set off will also be expired. Inability to carry forward such losses may affect your future income determination and taxes.

Conclusion

Many people find themselves wondering about the differences between the old and new tax regimes. The new income tax regime is designed to accommodate those who have more personal commitments, such as repayment of personal/vehicle loans, medical treatment of parents or dependents, or wish to avoid the burden of extensive tax preparation, or have minimal tax deductions due to their ineligibility for section 10 exemptions, standard deductions, tax on employment, employer contribution to pension scheme, etc. Senior adults, who get a significant amount of their income from interest, might benefit from Section 80 TTB, which allows them to claim Rs.50,000 as an interest income deduction and feel more safe under the old tax regime.

Both old and new tax regimes have advantages and downsides. The prior tax structure encourage taxpayers to save, whereas the current tax structure benefits employees with lesser wages and assets, resulting in fewer deductions and exemptions. The new tax system is seen as safer and simpler, with fewer records and a lower risk of tax evasion fraud. However, because to the unique nature of individual deductions and exemptions, a detailed comparison of the two regimes is required to decide which is best for each person.

Related Articles:

How to File ITR Through CA/Tax Expert?